How to Improve Cash Flow in Your Business

Improving your cash flow isn’t some tricky accounting idea, it’s about making sure you have more money coming into your business than going out over a certain time. It’s the day to day work of getting paid faster, watching what you spend, and keeping enough cash in the bank to run things without constantly looking […]

By Matthew Clarkson · December 8, 2025

Improving your cash flow isn’t some tricky accounting idea, it’s about making sure you have more money coming into your business than going out over a certain time. It’s the day to day work of getting paid faster, watching what you spend, and keeping enough cash in the bank to run things without constantly looking over your shoulder.

The fastest structural fix is invoicing that never waits for a human. See how invoices that raise themselves work when billing is wired to the job itself.

Why Healthy Cash Flow is Your Business Lifeline

Think of cash flow as the fuel that keeps your business running. You might have a powerful engine, a profitable company, but without fuel in the tank, you’re not going anywhere. This is a classic trap. Many businesses get fixated on profit, which is simply the money left over after all expenses are paid.

Profit is vital, of course, but it’s a long term measure of success. Cash flow is the immediate reality. It’s the actual cash you have on hand to pay your team, your suppliers, and the rent. A highly profitable business can easily go under if its clients take too long to settle their invoices.

For Australian small and medium businesses, this has become a major focus. Recent data shows the share of these businesses seeing better cash flow increased by 1.3% in the first quarter of 2025, marking the second straight quarterly improvement. It’s a positive sign that suggests things are starting to stabilise for many local businesses.

The Difference Between Profit and Cash Flow

It’s absolutely critical to understand that profit and cash are not the same thing. You can be profitable on paper and still have an empty bank account.

Here’s a simple way to think about it:

- Profit is what you earn. It’s your total sales minus your total costs for a given period.

- Cash Flow is what you have. It’s the actual money moving in and out of your accounts.

A key part of understanding your financial health is getting to grips with reports like the Profit and Loss (P&L) statement. While your P&L shows profitability, your cash flow statement tells the real story about your available cash.

Imagine you run a catering business. You land a huge event and invoice the client for $20,000. Your P&L for that month looks fantastic. But if the client has 90 day payment terms, you won’t see that cash for three months. Meanwhile, you still have to pay your staff and food suppliers this week. That gap is a cash flow problem.

This is exactly why looking only at profit isn’t enough. You have to actively manage the timing of your cash to stay in the game.

Quick Wins to Boost Your Cash Flow Today

Before diving into complex strategies, there are often simple, immediate actions you can take to see a rapid improvement. We’ve seen these tactics work for countless businesses, and they don’t require major investment.

| Tactic | What It Means | Why It Helps |

|---|---|---|

| Review Payment Terms | Shorten your standard invoice terms from 30 days to 14, or ask for a deposit upfront. | This immediately speeds up the flow of cash from new sales and projects. |

| Send Invoices Faster | Don’t wait until the end of the month. Invoice clients the moment work is completed. | The sooner the invoice is sent, the sooner the payment clock starts ticking. |

| Offer Early Payment Discounts | Give a small discount (e.g., 2%) for clients who pay within 10 days. | It encourages quick payment, turning your accounts receivable into cash much faster. |

| Chase Overdue Invoices | Set up a consistent follow up process for any invoice that goes past its due date. | This stops small delays from turning into large, problematic debts. |

These small adjustments can make a surprising difference to your bank balance in just a matter of weeks. They’re all about creating a sense of urgency and making it easy for your customers to pay you promptly.

Strategies to Get Paid Faster

Waiting on unpaid invoices feels like running a business with the handbrake on. You’ve done the work, you’ve delivered the value, but the money simply isn’t in your account. The real secret to improving your cash flow often comes down to one thing: shrinking that waiting period. It isn’t about being aggressive; it’s about being clear, efficient, and making it dead simple for your clients to pay you.

Even small, seemingly minor tweaks to your invoicing and collections process can have a huge impact. Think of it like a pipeline. A few small leaks or blockages can slow the entire system to a crawl. By tightening up each stage, you ensure cash flows through smoothly and quickly, keeping the business healthy and ready for whatever comes next.

Rethink Your Invoicing Process

Your invoice is more than just a bill, it’s a call to action. Is yours as clear as it could be? A confusing or incomplete invoice is just an invitation for delay. The moment the work is complete, that invoice should be on its way. Waiting until the end of the month is an old habit that directly harms your cash position.

To make an immediate difference, check that every single invoice includes:

- A clear due date: Phrases like “Due upon receipt” are vague. Use a specific, unmissable date.

- Multiple payment options: Don’t make them hunt for it. Offer bank transfer, credit card, and other online payment methods right there on the document.

- Itemised descriptions: Clearly list the services or products provided to prevent any questions that might hold up payment.

- Contact details for queries: Make it easy for clients to get answers without putting the invoice in the “too hard” basket.

We worked with a creative agency whose average payment time was a painful 60 days. By simply redesigning their invoice for clarity and sending it the same day a project was signed off, they cut that average to just 32 days in a single quarter. That simple change injected a massive amount of predictable cash into their operations.

Automate the Follow Up Process

Let’s be honest, chasing late payments is awkward for everyone involved. It can strain client relationships and pulls your team away from more valuable work. This is exactly where automation becomes your best friend.

Setting up automated reminders is a simple but powerful way to get paid on time. Instead of relying on manual follow ups, a system can send out polite nudges on a set schedule. Imagine a friendly email three days before the due date, another on the day it’s due, and then a series of firmer (but still professional) reminders if it becomes overdue. This consistency ensures nothing slips through the cracks and it also depersonalises the process, making it far less confrontational. To see how this fits into a bigger picture, you can explore the power of sales automation and its applications in financial workflows.

Incentivise Early Payments

What if you could actually encourage clients to pay you faster? Offering a small discount for early payment can be an incredibly effective tool. A typical offer is a 2% discount if the invoice is settled within 10 days, on what might otherwise be 30 day terms.

Sure, you lose a tiny percentage of the revenue, but you gain immediate access to your cash. That trade off is often well worth it, as it reduces your need to dip into credit lines to cover operational expenses. It also gives you a great way to identify your most reliable, top tier clients. And for businesses that frequently deal with payment disputes, exploring specific chargeback representment strategies can also significantly improve cash recovery and protect your revenue.

Managing Expenses Without Slowing Growth

When cash feels tight, the gut reaction is often to start slashing expenses everywhere. But that’s like trying to make a car lighter by ripping out the engine. Cutting costs shouldn’t mean cutting off your path to growth. The real goal is to spend smarter, not just less, and make every single dollar work harder for the business.

Think of it as a strategic financial health check. You’re not just hunting for things to eliminate; you’re looking for inefficiencies and chances to get more value for your money. This approach lets you protect the crucial investments that fuel your future while trimming the fat from areas that no longer serve you. It’s a delicate balancing act, but getting it right is fundamental to building a resilient business.

This isn’t just a theoretical exercise. According to a recent CommBank survey, nearly 80% of Australian small and medium businesses felt some impact on their cash flow in the last year alone. In response, reviewing and decreasing expenses was one of the most common strategies businesses used to stay on track. You can read the full UNSW analysis of the cash flow challenges facing Aussie businesses.

Conduct a Ruthless Expense Review

First things first: you need a crystal clear picture of where your money is actually going. This means going through your expenses line by line, paying special attention to the recurring ones that can easily fly under the radar. Software subscriptions, service contracts, and old memberships can add up to a significant sum over time.

For each expense, you have to ask a simple question: “Is this absolutely essential for generating revenue or keeping the lights on?” You’ll almost certainly find services you signed up for years ago that are no longer being used, or platforms where a cheaper alternative would do the job just as well.

This isn’t about being cheap; it’s about being intentional. A business we worked with was paying for premium licences for a project management tool for its entire 50 person team. A quick audit revealed only 10 people were actively using the advanced features. By switching the other 40 users to a basic plan, they saved thousands a year without impacting productivity at all.

This kind of forensic review often uncovers easy wins that free up cash almost instantly. It’s about optimising, not just cutting.

Negotiate Better Terms with Your Suppliers

Your relationship with suppliers is a two way street, not just a series of transactions. Just as your clients might occasionally ask for flexible payment terms, you can, and should, do the same with the businesses you buy from. A strong, long term partnership puts you in a great position to have these conversations.

Improving cash flow from your payments usually boils down to two key areas:

- Payment Terms: Can you extend your terms from 30 days to 45 or even 60? This simple change creates a bigger cash buffer to manage your own operations and sales cycles. It directly improves your Days Payable Outstanding (DPO).

- Pricing and Discounts: Are you getting the best possible price? If you’re a reliable, high volume customer, don’t hesitate to ask for a better deal. You could also explore discounts for bulk purchases if it makes financial sense for your inventory levels.

Never be afraid to ask. The worst they can say is no, but you’ll often find suppliers are willing to be flexible to keep a good customer happy. A 15 day extension on payments might not seem like much, but when applied across all your major suppliers, it can create significant breathing room in your cash reserves.

For tackling more complex challenges and identifying deeper efficiencies, working with expert AI consultants can help automate financial analysis and pinpoint hidden opportunities for savings you might otherwise miss.

Using Technology to Optimise Cash Flow

Think of the right technology as a tireless financial analyst for your business. It works around the clock, handles the boring tasks flawlessly, and gives you crystal clear insights into your cash position. This isn’t about jumping on the latest tech trend. It’s about using proven tools to gain genuine control over your money and make smarter decisions that improve your cash flow.

Relying on manual processes is like trying to direct peak hour traffic with hand signals. Inevitably, things get missed, mistakes creep in, and the whole system slows to a crawl. Technology brings in the traffic lights and automated controls, ensuring everything flows smoothly. It drastically cuts down on human error and, just as importantly, frees up your team to focus on work that actually requires their expertise.

Automate Your Billing and Collections

One of the biggest drags on cash flow is the lag between finishing a job and getting paid. This is a perfect candidate for automation. An automated billing system can generate and send an invoice the very moment a project is completed or a product is shipped, kicking off the payment cycle immediately.

There’s no more waiting for someone to run a batch at the end of the month or letting invoices pile up on a desk. The system just gets it done.

Beyond that, you can set up automated payment reminders that follow a consistent, professional schedule. These systems can send polite but firm messages at set times, such as:

- A friendly heads up a few days before the due date.

- A notice on the day the payment is officially due.

- A sequence of follow ups if the invoice becomes overdue.

This kind of persistence ensures nothing slips through the cracks. It also removes the awkward and time consuming task of having your team chase clients for payment, professionalising the entire process and getting cash in the door far quicker.

It’s a sobering fact that a huge number of business failures can be traced back to poor cash management. Automation tackles this head on by creating a predictable, reliable collections process that doesn’t rely on someone remembering to make a call.

Get a Real Time View of Your Finances

How can you possibly make good decisions when you’re looking at old data? Many businesses still operate off manual reports that are already out of date by the time they land on a manager’s desk. The right technology completely changes this by integrating your core systems, your accounting software, CRM, and ERP.

The result is a live dashboard for your company’s financial health. When your sales team closes a deal in the CRM, that information flows straight into your accounting platform. When a customer pays an invoice, your cash forecast updates instantly.

This creates a single source of truth, giving you an accurate, real time picture of your cash position. You can see precisely what’s coming in, what’s going out, and what your balance will look like next week or next month. This allows you to shift from being reactive to proactive, spotting potential cash shortfalls long before they ever become a crisis. A great starting point for building this kind of connected system is to explore options for automated data processing.

Make Smart Investments in Technology

Investing in technology isn’t just another expense. It’s a strategic move to build a more efficient and resilient business. Recent figures on Australian businesses reveal a telling trend: investment in equipment and financing is growing at more than triple the rate of working capital. This shows that smart companies see technology as a fundamental driver of better cash flow and long term stability. You can dig deeper into how local businesses are investing in the latest national accounts data.

To help you map out where to begin, it’s useful to compare the common technology solutions available.

Cash Flow Tech Solutions Compared

| Technology | Primary Benefit | Best For |

|---|---|---|

| Billing & Invoicing Software | Dramatically speeds up the time it takes to get paid by automating invoice creation and reminders. | Businesses of all sizes, especially those with high transaction volumes. |

| Expense Tracking Apps | Gives you instant visibility into spending and massively simplifies reimbursement processes. | Companies with teams that regularly incur business related expenses. |

| Cash Flow Forecasting Tools | Uses historical data and AI to predict future cash positions with a high degree of accuracy. | Medium to large businesses looking to make more strategic financial moves. |

| Integrated ERP/CRM Systems | Creates a single source of truth for all financial and customer data across the organisation. | Large businesses needing to connect multiple departments and functions. |

Ultimately, choosing the right tools provides the visibility and control you need to navigate financial challenges with confidence. It transforms cash flow management from a source of constant stress into a powerful strategic advantage.

Building Your Cash Flow Improvement Plan

https://www.youtube.com/embed/9wAa9oZ1Z6o?feature=oembed

Knowing what to do is half the battle; actually doing it is what moves the needle. All the strategies we’ve covered are powerful, but they only deliver results when you have a clear, actionable plan to bring them to life. This is where you build your roadmap, a practical guide to get from where you are now to where you need to be.

Think of it like planning a major project. You wouldn’t just start building and hope for the best. You’d map out the destination, chart the route, and define the key milestones. Your cash flow improvement plan is no different. It’s not about trying to do everything at once. It’s about being strategic, focusing on the changes that deliver the biggest return on effort, especially in the early days.

Prioritise Your Actions for Maximum Impact

Before you dive in, you need to decide what to tackle first. It’s easy to feel overwhelmed by all the possibilities, so ruthless prioritisation is your best friend. The goal here is to identify the “quick wins” that build momentum and free up cash fast, giving you the breathing room to work on bigger, more complex projects.

Start with one simple question: “What’s our single biggest cash flow headache right now?”

- Are clients taking forever to pay? Your immediate priority should be your invoicing and collections process.

- Are supplier payments draining your accounts before customer cash arrives? Renegotiating terms with your key vendors should be top of the list.

- Is your team swamped with manual financial admin? Exploring automation technology is where you need to focus your energy.

By pinpointing the most significant pain point, you ensure your initial efforts are directed where they’ll make the most tangible difference.

For many businesses, the fastest gains come from tightening up the accounts receivable process. It’s a common blind spot. Across various industries, nearly 50% of invoices are paid late. Fixing this one issue can unlock a significant amount of cash that’s rightfully yours but is stuck in limbo.

Setting Clear Goals and Tracking Progress

A plan without clear targets is just a wish list. To make your efforts count, you need to set measurable targets, often called Key Performance Indicators (KPIs). These are the numbers that tell you, without ambiguity, if your plan is actually working. A vague goal like “get paid faster” won’t cut it.

A solid KPI, for instance, would be: “Reduce our Days Sales Outstanding (DSO) from 45 days to 30 days within the next 90 days.” This target is specific, measurable, achievable, relevant, and time bound (SMART). It gives you a clear finish line and a timeframe to get there.

Tracking these metrics is non negotiable. It’s the feedback loop that tells you what’s working and what needs adjusting. It’s also worth exploring how different tools can work together to give you a more unified view of your operations through effective system integrations.

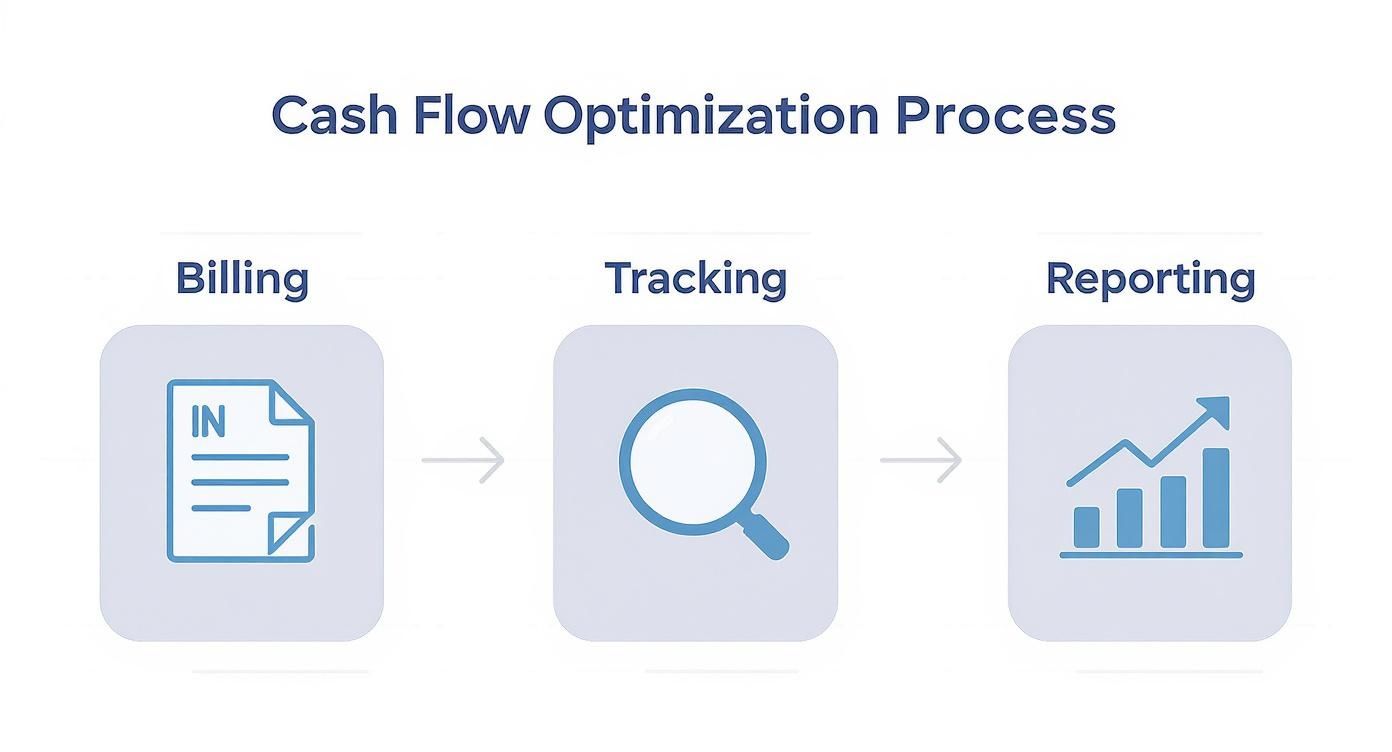

This diagram outlines the core process for getting your cash flow in order, from billing right through to reporting.

As you can see, effective cash flow management is a continuous cycle, not a one time task.

A Practical 90 Day Plan Example

Let’s walk through a real world scenario. Imagine a mid sized construction company that’s profitable on paper but always seems to be scrambling for cash. Here’s what their first 90 day improvement plan could look like.

Month 1: Focus on Invoicing and Collections

- Week 1: Redesign the invoice template. Make due dates bold, add multiple online payment links, and include direct contact details for the accounts team.

- Week 2: Implement a new policy: invoices go out the same day a project stage is completed. No more waiting until the end of the month.

- Week 3: Set up automated reminders to gently nudge clients a few days before an invoice is due and follow up on overdue payments.

- Week 4: Review the initial results. How have payment times been affected?

Month 2: Focus on Supplier Management

- Weeks 5-6: Identify the top five largest suppliers by spend. Open conversations about extending payment terms from 30 days to 45 or even 60 days.

- Weeks 7-8: Research alternative suppliers for non critical materials. Can you get better pricing or more favourable terms elsewhere?

Month 3: Focus on Technology and Reporting

- Weeks 9-10: Trial an expense tracking app to get real time visibility on project spending by the site teams.

- Weeks 11-12: Build a simple weekly cash flow dashboard to track key metrics like DSO, DPO, and cash on hand.

This phased approach keeps the process from becoming overwhelming and allows each stage to build on the success of the last.

Frequently Asked Questions About Cash Flow

We hear a lot of the same questions from leaders trying to get a better handle on their cash flow. Getting clear answers is often the first step towards a stronger financial position, so we’ve answered some of the most common queries that come our way.

What’s the Fastest Way to Improve Cash Flow?

The quickest win nearly always lies in your accounts receivable. This is cash that’s already yours; it’s just sitting in someone else’s balance sheet. The single best tactic is to send out your invoice the moment a job is done or a product has been delivered. Don’t fall into the trap of waiting for a monthly billing cycle.

Make sure your invoices are crystal clear, completely accurate, and feature simple, unmissable payment instructions. You’d be surprised how often a polite but firm follow up on the day an invoice is due makes a difference. This isn’t about being heavy handed; it’s about signalling that you run a tight ship and expect to be paid on time.

Chasing late payments can feel awkward, but it’s a non negotiable part of business. Remember, you’ve earned that money. A simple, automated email reminder system can take the personal element out of it, keeping the process professional and stopping small delays from snowballing into big problems.

How Should I Manage Cash Flow When Sales Are Down?

When revenue dips, the game shifts from speeding up incoming cash to carefully managing outgoing payments. It’s time to put on your detective hat and check every single line item. A great place to start is with recurring expenses like software subscriptions or memberships. Do you really need all of them right now?

This is also the perfect opportunity to talk to your key suppliers. Don’t be afraid to ask if they can extend your payment terms, perhaps from 30 days to 45 or even 60. Many suppliers would much rather offer a good client some flexibility than risk losing their business entirely. It also pays to have a pre-approved business overdraft or line of credit in place; it can act as a vital safety net to cover essentials until sales bounce back.

Is Taking on Debt a Bad Way to Handle Cash Flow?

Not necessarily, provided it’s done strategically. Using debt to plug fundamental leaks in your business model is a dangerous game. It’s the financial equivalent of bailing out a leaky boat with a bucket instead of fixing the hole.

However, using debt to fund growth is another story entirely. It’s often a very smart financial play. Think of it like this:

- A working capital loan could allow you to buy inventory in bulk at a steep discount, immediately boosting your profit margins.

- Financing new equipment that makes your team more efficient means you can produce more in less time, which flows directly to your bottom line.

The acid test is whether the debt generates more value and revenue than it costs in interest. It has to be an investment in your future, not just a plaster on a present day wound.

How Often Should I Forecast My Cash Flow?

The right timing really depends on where your business is at. For most stable, established companies, running a detailed cash flow forecast once a month hits the sweet spot. This gives you a solid read on your financial rhythm without getting lost in the weeds.

But that all changes if your business is going through a dynamic period. If you’re in a high growth phase, navigating extreme seasonal shifts, or facing market uncertainty, switching to a weekly forecast is a much smarter move. The whole point is for your forecast to be a living document. It should be a practical tool that actively guides your decisions, not just another report that gets filed away.

At Osher Digital , we specialise in building automated systems that provide real time visibility and control over your finances. If you’re ready to shift from reactive problem solving to proactive financial strategy, speak with our expert AI consultants to see how we can help.

Last updated on August 6, 2026

Free tool · 2 minutes

Automation ROI Calculator

See what a manual process is really costing you, and the payback on automating it.

Continue Reading

View all

Rented software was always a compromise. AI has ended it.

Off-the-shelf software made sense when custom cost $250,000. AI-assisted development changed the maths. Why we now build software around the business, AI-first, and connected to Claude and ChatGPT, starting at $15k.

Aug 6, 2026

n8n Outlook Automation: Where the Node Stops and Graph Begins

n8n Outlook automation breaks in predictable places: subfolders, attachments, shifting email IDs, plus the Graph API workarounds we run in production.

Mar 16, 2026

What Is a Workflow? Definition, Parts, and What Breaks

A workflow is the repeatable set of steps that takes a task from start to finish. Here is what a workflow is made of, and the parts that quietly break.

Mar 1, 2026

Sick of reading about automation?

Book a free 15-minute intro call. We’ll talk through what you’re trying to automate and whether we’re a good fit.